E-Newsletter

FCEDA forum spotlights access to capital for minority-owned businesses

Minority entrepreneurs face challenges in accessing capital to start, grow and sustain businesses, and that problem has worsened during the economic downturn caused by the COVID-19 pandemic. The Fairfax County Economic Development Authority (FCEDA) and the Northern Virginia Economic Development Alliance addressed the issue in an August 21 virtual forum, “Access to Capital for Minority-Owned Businesses.”

(Click on link to download a recording of the event, or watch the recorded webinar below.)

Moderated by Victor Hoskins, FCEDA’s president and CEO, the forum drew more than 300 attendees and featured a discussion with U.S. Sen. Mark Warner of Virginia; Staci Redmon, founder, president and CEO of Fairfax County-based Strategy and Management Services, a minority, woman and service-disabled veteran-owned business; B. Doyle Mitchell, Jr., president and CEO of Industrial Bank in Washington, D.C.; and Ellis Carr, president and CEO of Arlington-based Capital Impact Partners.

With the focus on providing actionable solutions for small business owners from the public and private sectors, the panelists discussed efforts to ensure access to government-backed funding programs for minority-owned firms; what the financing community can do to close the gap regarding access to capital; and how minority entrepreneurs can best position themselves to increase their chances of being funded.

Redmon cited statistics showing how Black-owned businesses have been affected by the pandemic. “There were more than one-million Black-owned businesses in the U.S. at the beginning of February, according to research from the University of California at Santa Cruz which drew from Census survey estimates,” she said. “By mid-April, 440,000 Black business owners had closed their companies for good. This is a 41 percent plunge. By comparison, 17 percent of White-owned businesses closed during the same time.”

Warner, a member of the Senate Banking, Housing, and Urban Affairs Committee, noted his background as a business owner and investor. He discussed legislation that he introduced last month, the Jobs and Neighborhood Investment Act, S.4255, which calls for $17.9 billion in investment in low-income and minority communities hard hit by COVID-19. It has been co-sponsored by six Democratic senators and seven Republican senators.

The legislation would establish programs to revitalize and provide long-term financial products and services to invest in, low- and moderate-income and minority communities, and enhance the stability, safety and soundness of community financial institutions that support low- and moderate-income and minority communities.

Many Black, Brown- and woman-owned business people have to “bootstrap” their businesses — start and fund their operations themselves — because they don’t have a relationship with a financial institution, he said. “That’s really what black and brown and women-owned businesses do because they can’t get access to capital, so they have to go out and go into their 401K, or mortgage their house, or borrow from friends and family,” he said.

Companies without a good relationship with a bank had problems getting approved for the Paycheck Protection Program established by the federal government this year to help businesses bridge the economic downturn caused by the coronavirus pandemic, Warner said.

“When the data is fully out, the [Paycheck Protection Program] PPP, one of the largest programs that the federal government ever put together, with close to $600 billion, the take-up rate amongst black and brown businesses will be really small because if you use the banking system as the distribution mechanism and you don’t have a previous banking relationship then you didn’t get called,” Warner said. “I don’t even fully blame the banks. They were trying to get the money out as quickly as possible so they were going to their customers first.”

Warner also noted that less than 3 percent of venture capital investments go to Black or Brown-owned entrepreneurs, and less than 10 percent go to woman-owned businesses.

Redmon said economic recovery needs to be approached with “a strong equity lens particularly at a time when small minority-owned companies may be most at risk in the wake of COVID-19.”

Redmon said she was able to obtain a PPP loan and EIDL [Economic Injury Disaster Loan], but she expressed concern that she may have to dip back into her personal 401K to save the business, as she had to do to start the business in 2008.

“When it came to the PPP, the large banks processed PPP loans that were favored with whom they had pre-existing relationships. This left many minority-owned companies like mine on the sidelines,” Redmon said. “Minority businesses like mine will continue to be disenfranchised until we connect with the Black and minority communities where they are and commit to legislation that is specifically focused on serving the financial needs of minority-owned businesses.”

Mitchell advised business owners to establish relationships with banks in order to increase their chance of obtaining capital.

Industrial Bank is the largest minority-owned commercial bank in the Washington area and the sixth-largest African American-owned financial institution in the country. The bank was founded by Mitchell’s grandfather in the U Street corridor of Washington in 1934, and Mitchell led the Bank into Prince George’s County, Md., in 1994.

“There have been many challenges for small businesses throughout history and certainly race is one of them,” Mitchell said. “But those challenges have been really, really heightened during this crisis. And I think it caught a lot of small businesses off guard.”

Small businesses that seek funding should establish a relationship with both a large bank and a small bank, Mitchell advised. “You definitely need a bank that knows you and you can feel that they care about you and your business.”

“When the PPP hit, all the banks and institutions tried to serve their customers… And then even some of the larger banks stopped serving their customers,” according to Mitchell. “And so this is why you need [relationships with] more than one institution, in my opinion, because you may get different things from different institutions.”

Carr focused the need to drive capital to business owners in communities of color. Capital Impact Partners is a certified community development financial institution that provides credit and financial services to under-served markets and populations in the United States.

“Since our founding almost four decades ago, we’ve invested about $3 billion in communities across the country to really support social and economic justice issues,” Carr said. “And while we’re proud of the work that we’ve done and the impact we’ve had in communities, we realized that we needed to pivot because despite our efforts, many communities, particularly communities of color, are faring much worse than they did 10 years ago.”

In response to the pandemic, Capital Impact Partners recently announced a partnership with CDC Small Business Finance, an SBA lender, to “drive scale capital in a holistic community and economic development fashion with a specific focus on communities of color,” according to Carr.

“One of the things that really the pandemic has shown is the lack of connection between institutional and broader capital and black and brown communities,” he said.

“The Fairfax County Economic Development Authority was proud to be able to hold a timely event on this important topic, and we are so thankful to have experts in this region who can address it,” said Victor Hoskins, president and CEO of the FCEDA. “Minority business owners should have equitable access to capital in order to start, grow and maintain their companies–a need which has been heightened exponentially during the pandemic.”

In Fairfax County, 41 percent of all businesses are minority-owned. That includes more than 600 African-American-owned businesses with payrolls. These companies generate $1.8 billion in annual revenue. Click here to view a downloadable list of Resources for Minority Businesses at the local, regional and national levels from a wide variety of organizations and agencies.

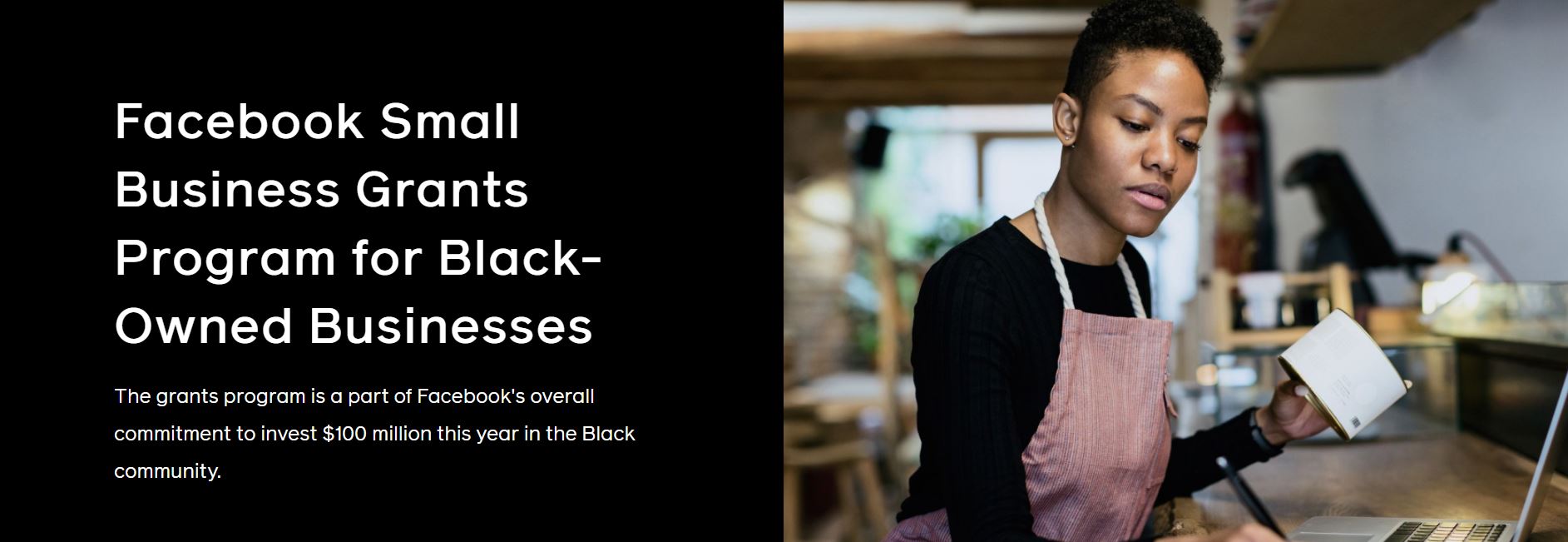

Facebook Establishes Black-owned business grant program

Facebook, which announced in 2019 that it would open an office in Reston, has established a Black-owned business grant program for up to $4,000 in funding.

Eligible businesses must be a majority Black-owned, for-profit business, be legally registered in a U.S. state or the District of Columbia, have between one and 50 employees, have been in business for more than one year, have experienced challenges from COVID-19 and plan to use grant funds to support the business and community.

The application will be open through Aug. 31 and funds will be awarded “as quickly as possible,” according to Facebook. Facebook is partnering with Accenture to administer the program, and AEO is offering strategic advisory services for serving diverse businesses. Find out more in Virginia Business.

August 27, 2020

News Travels Fast

Stay ahead of the curve with the latest business news from Northern Virginia. Receive updates on moves, incentives, workforce, events and more.